The past few months have shown that certain implementations of algorithmic stablecoins with various percentages of backing aren’t scalable. Because of this, we’re extremely happy to be supporters of Gyroscope - a dynamic stablecoin protocol that is fully collateralized and decentralized. We believe that they are building out a protocol with extreme fortitude that can persistently support a decentralized stablecoin through a wide range of eclectic events. In addition, we are convinced that decentralised stablecoins are one of the best use cases of crypto. We first met the Gyroscope team in January 2021, after reading their research papers online. After extensive back and forth we are proud to have partnered with them on building out the Gyroscope project from the earliest days and into the future.

To understand how Gyroscope is trying to revolutionize the way stablecoins currently function, it’s important to first take an in-depth look at how stablecoins have progressed over the years and what sets them apart from each other. First, let’s start with the history of stablecoins and then move down to the various types of stablecoins that exist and some of the death spirals that can arise.

First off, let’s establish what a stablecoin is. A stablecoin is a cryptocurrency that is supposed to remain stable in value against a pegged external asset (usually USD). It should aim to minimize price volatility (in relative terms to the value of USD), either through full collateralization or other methods. The purpose of stablecoins is usually to negate the speculative nature of crypto and create a market for USD/Token markets on DEXs.

The history of on-chain stablecoins started on a hot summer day in June 2014, when the first on-chain stablecoin was released — bitUSD on the BitShares blockchain. Suppose you’re familiar with the olden days. In that case, you might remember some of the people that were behind BitShares, such as Daniel Larimer of EOS fame and Charles Hoskinson, the champion fast eater.

So how did BitUSD work? Well, it actually worked in a similar way to some of the “algo” stablecoins of recent years, let me explain.

One could redeem and mint BitUSD, however, the price of this transfer was determined by the BitUSD vs BitShares price in a distributed exchange, which is not linked to actual green American dollars. As such the price references itself and tries to fix its peg on the basis of arbitrage. The only argument of why BitUSD should trade at $1 is thus “why would it be anything else, it’s a stablecoin?” — Which is very much the same reason as with the UST debacle.

In this situation, should the value of the collateral currency (in this case Bitshares) fall, any BitUSD holder could redeem and gain $1 worth of BitShares. However, this assumes that the market price of BitUSD is still worth $1 and there are sufficient Bitshares in collateral. So, not quite the same as LUNA/UST (Where UST was always redeemable for $1 of LUNA). Regardless, the same issues that UST was presented with, also existed way before that, even back in 2014. And if you’re wondering how the story of BitUSD and NuBits turned out — well you can check the charts, it will show a very similar story to the Luna debacle.

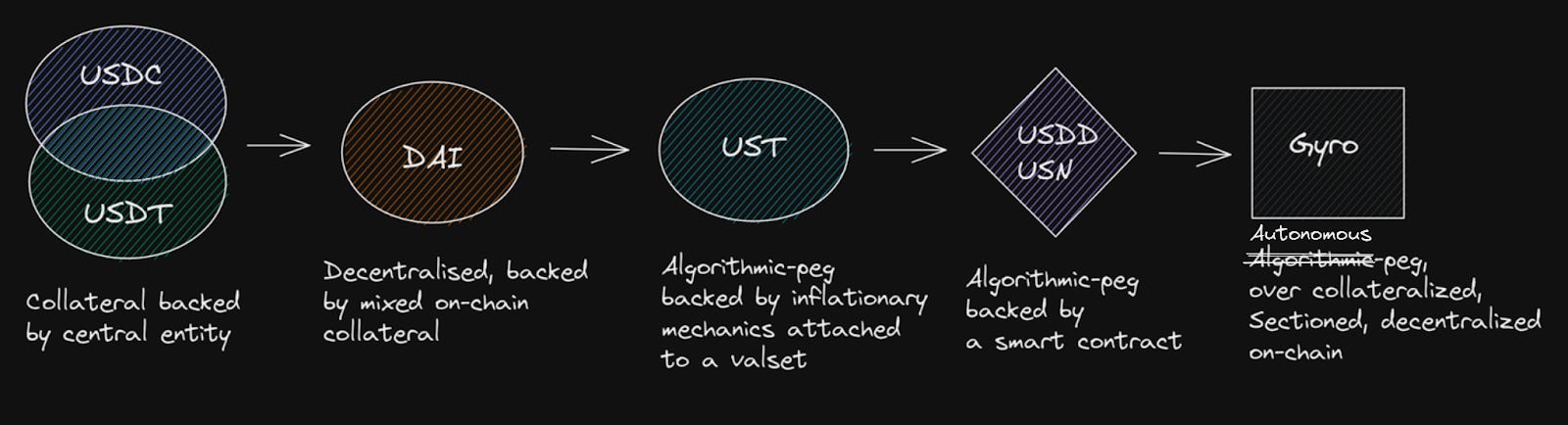

One of the earliest stablecoins, that even to this day has kept its peg is USDT (Tether). It came to the market in 2015 via Bitfinex. USDT is an off-chain collateralized on-chain stablecoin, backed by real assets and to this day is the most popular stablecoin in existence (MKT cap at ~$67.5B). Tether has seen various events and has had controversies around it since its inception. However, despite all of that, it has managed to keep its peg and become one of the go-to stables alongside USDC, for people seeking to offload risk.

While Tether has been useful in solving liquidity issues, it brings a key fundamental issue that blockchain was intended to solve into the space: centralisation. DAI was created to solve this centralisation issue (although it is still relatively centralised). However, it brought its own unique problem — namely, during contractionary (and sometimes expansive) market events (i.e., market volatility), DAI could lose its peg to the $USD when the collateral which backs DAI (principally ETH) was liquidated. As a result, DAI is currently backed by around ˜75% USDC and is therefore almost a decentralized derivative of USDC itself, backed by some volatile assets such as ETH.

Tantamount to algorithmic and essentially unbacked stables, TerraUSD’s algorithmically pegged stablecoin was a design that allowed for dynamic adjustments to market forces in real-time like the ones used in BitShares with some changes, eventually leading to its downfall.

So let's summarise the type of stablecoins that are currently in existence and input them into a diagram to see their differences.

Under this section lies the two most popular stables, namely USDC and USDT which have a combined market cap of ~$119B. These are backed by real-world collateral held by a central entity, and in some cases frequently verified by external auditors. Keep in mind that in most cases these types of stables are often backed by both fiat and commodities among other trad-fi instruments.

These are stables that are backed by other on-chain cryptocurrencies and in some cases even backed partly by off-chain collateralized stables, such as with DAI. The peg is executed on-chain via smart contracts and is at the mercy of arbitragers to keep the peg safe, and for watchers/searchers to liquidate collateral when it reaches liquidation. Some of the collateralized on-chain stables are also backed by yield-generating assets, such as in the case of MIM and YUSD.

This is usually referred to as seigniorage style stables, which use algorithms to control the money supply of the stablecoin, often through an asset held by the entity issuing the stable itself. You can compare this type of stable to a central bank printing and destroying the currency, but on a global decentralized scale. In most cases, there is no collateral (unless raised to back the peg, as with Luna’s or Tron’s reserves) and the peg is defended by mints/burns made on-chain via arbitrage hunters through a system that in Luna’s case had an internal asset be the primary risk absorber, which in a death spiral event led to the hyperinflation of said asset.

To give a better overview of where the various stablecoins land in regards to their risk absorption and primary value let’s plot them into a table.

This makes it very clear that there’s a large variety of stablecoins currently on the market, with the primary ones being USDT/USDC which are both backed by a central entity. The only decentralized stable that’s somewhat close, albeit one order of magnitude smaller, is DAI, which has a market cap of around ~$6.4B. MakerDAO has recently had discussions about moving away from a principal backing of USDC towards more decentralized assets, such as ETH, which certainly makes for an exciting development. UST was the only decentralized stable, that was getting close to the market caps of the two large centralized ones. However, that was not to last.

The problem with many of the fallen stablecoins over the years is the fact that when investor panic occurs, which can be caused by varying events in the market, it causes a “death spiral” and the stablecoin loses its peg and with it the trust that it had.

Another great example of such an event is the fall of Basis Cash which at its peak had a meagre market cap of $30m. Basis Cash also utilised a seigniorage algorithm, as previously mentioned. In which there exists a stablecoin and a token that enforces the peg in the form of minting and burning - through arbitrage. There exist other examples, some of which tried to enforce a partial crypto-collateralized scheme, such as in the last months of UST. However, when the token enforcing the peg becomes overvalued and unable to enforce the ever-growing market capitalization of the stablecoin, it eventually leads to a death spiral such as with Luna and Iron.

Another major part of keeping the peg of a stablecoin is trust. A great example here is USDD by Tron. USDD is technically overcollateralized by the BTC and USDC/T held in reserve, however, it is permissioned and fully based on the belief that it will be used to uphold the peg. As of writing this, USDD is trading at 0.98(July), which clearly shows a distrust in the way the system is operating and the inability for the general public to participate in arbitrage.

Now that we have covered the history of stables, both successful ones and fallen ones, let's turn our eyes towards possible events that can impact a stables price ‘positively’, as in asset appreciation, and then we’ll move onwards to Gyroscope itself.

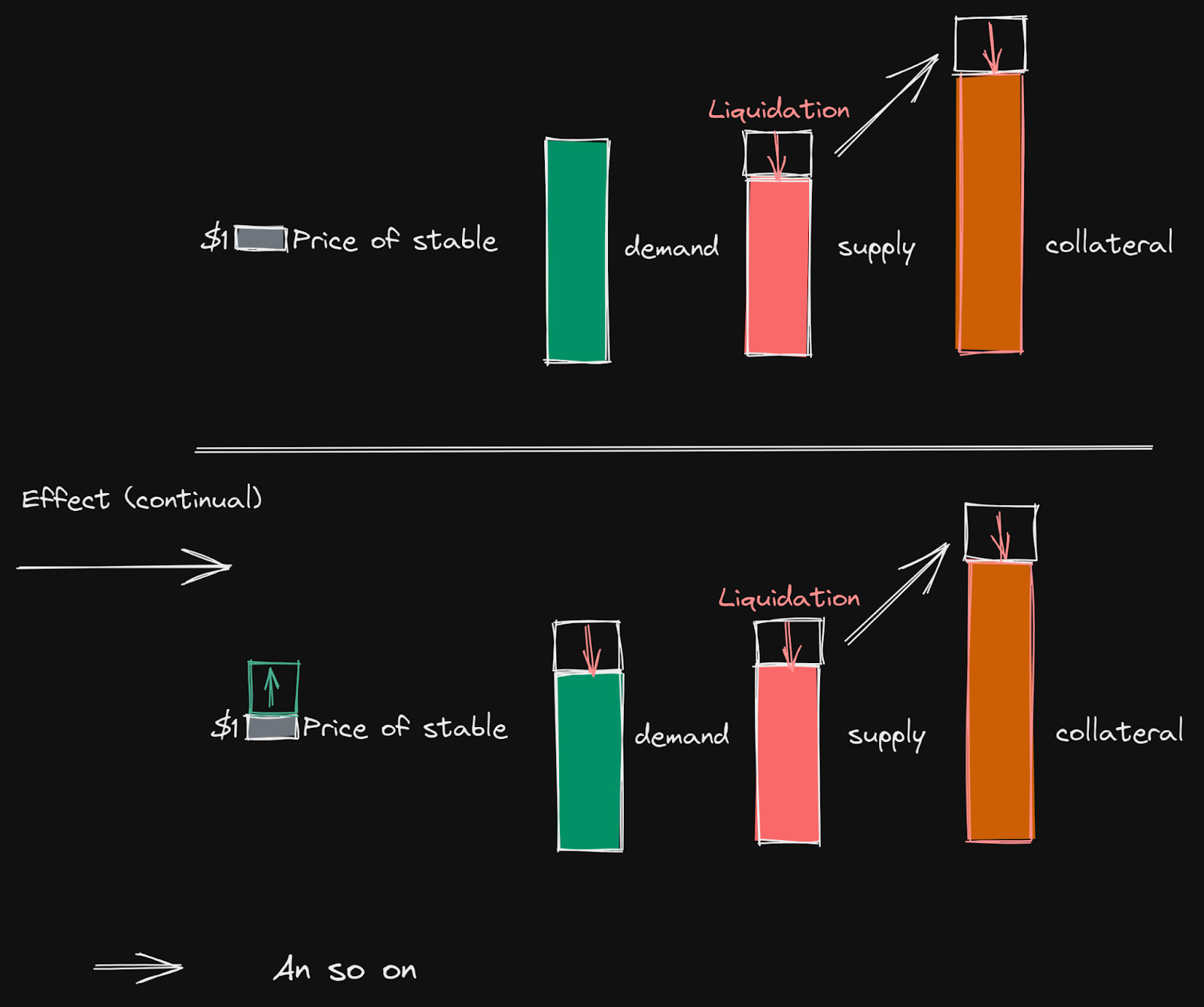

Deleveraging spirals are one of the ways that can lead to a stablecoin price appreciating, rather than keeping its peg as a result of arbitrage. This can happen during times of collateral shock and lead to faster collateral drawn.

When speculator liquidations begin to occur, as with for example DAI where it’s automated by the protocol or in a situation where voluntary deleveraging happens — collateral is used to repurchase the stablecoin to reduce the supply. If you’re interested in the exact way deleveraging spirals function and happen, you should check out Ariah’s work in this paper.

In elastic markets, this can have an adverse effect as it causes an imbalance in demand relative to supply. To combat the reduced demand, an increase in the stablecoins price is needed to reduce demand. This can further amplify the problem. In a situation where continual liquidations occur, more collateral is then needed to reduce supply by a similar amount to earlier because of the increased price of the stablecoin, and so on and so forth.

The speculator of the protocol will then most likely desire to increase collateralization when the expected liquidation cost is higher after a shock has hit the collateral value or if an expectation of volatility is anticipated. As such, the collateralization of DAI is exceptionally high. Often ranging between 2.5x to 5x, even though the collateral factor is actually 1.5x

Now that we have established the history of stables, the current market of existing stables and how a deleveraging spiral can occur, let’s dig deep down and understand how Gyroscope is trying to change the spectrum.

Gyroscope at its core is a protocol that allows for the minting of a meta-stablecoin. A meta-stablecoin is a stable that is composed of a basket of other assets, such as other stables, yield generating instruments or volatile assets. The basket of assets can then be used to acquire further yield.

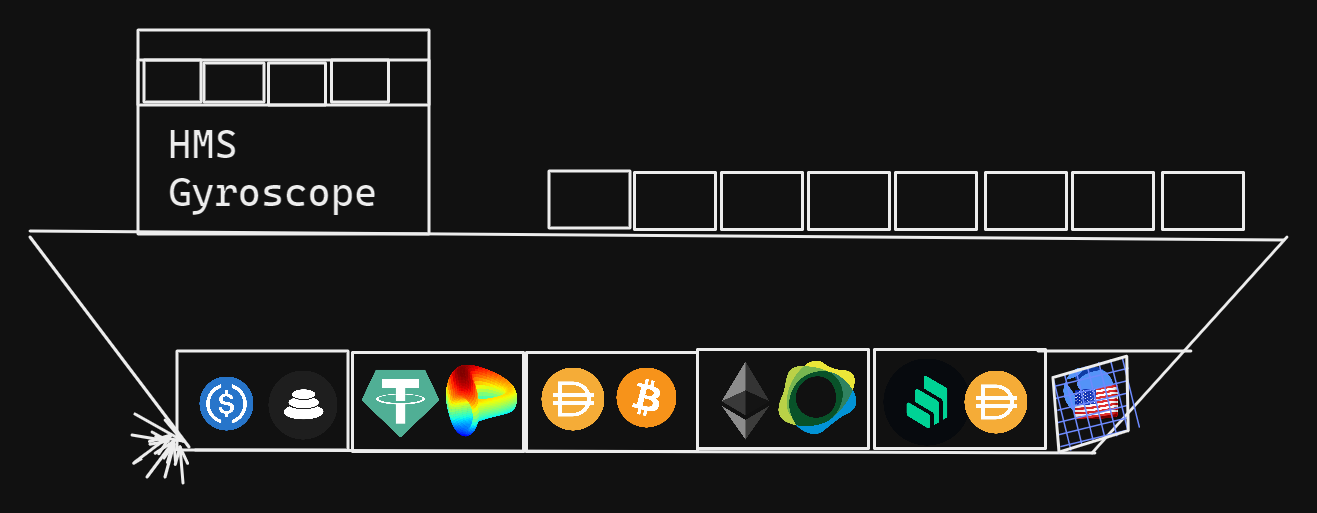

Gyroscope is unique in the sense that it is both collateralized and also has distinct defence mechanisms to restore the peg in the event of price downturns in currencies held in reserve. This is done through a method that is quite similar to the way ships work. For example, if there’s a hole in a ship, and a section of the ship gets flooded, the ship won’t sink. Why is that? Well, in most larger ships you have sections that can be blocked off in the case of flooding in one section. You can therefore limit the damage and spread of flooding by creating sections that can be blocked off. In the same vein, the stratified reserve of Gyroscope works similarly, let’s try to explain it with imagery.

Gyroscope is for all intents and purposes a fully-backed stablecoin since it aims to have a long-term reserve ratio of 100%. However, it has some more unique functionalities on top of that, which we’ll cover here. It has all-weather reserves and autonomous price bounding, to make sure that the price is as stable as possible. So what is an all-weather reserve? An all-weather reserve in this case is a basket of assets that collateralizes gyro. In the beginning, most of these will be other stablecoins, however, the reserve will eventually move to add other tokens too. When those are added, the reserve will diversify risks, to account for all possible events. Autonomous price bounding is when the prices for minting and redeeming stablecoins are set autonomously so that it balances the goal of a tight peg to exactly the USD. This is especially important during crises. We’ll go more in-depth with this shortly.

Arbitrage loop

Gyroscope, like basically any other stablecoin, has what we call an arbitrage loop. In Gyroscope's case, this is permissionless, unlike most centralized stablecoins. This is because the stablecoin itself is mintable with $1 worth of assets. When the price rises above peg, for example, more stablecoins can be minted and then sold on the market with proceeds. These proceeds can go to growing the reserve behind Gyro as well.

This also works the other way around. When there’s a drop in the stablecoin’s price, they can be bought on the market, and then redeemed for $1 worth of reserve assets. The arbitrage loop coupled with the all-weather reserve is the first line of defence in regards to keeping the peg of Gyro stable. This is something that has to happen permissionless, otherwise, the peg will never be arbitraged, just take one look at USDD. Furthermore, the peg cannot be restored purely with endogenous assets but has to be backed by exogenous assets too, hence the all-weather reserve of Gyroscope. In case of larger events and shocks to the reserve, more lines of defence exist to keep the peg and ensure stability. We’ll cover some more underneath.

Stratified Reserve

As mentioned earlier there are several lines of defence when it comes to keeping the peg of a stablecoin stable. The first one is the one described before, the stratified reserve that stores all issuance proceeds and diversifies risks in DeFi. The goal of this reserve is to keep a full collateralization ratio at all times. In the beginning, this will primarily be composed of stablecoins, but as sketched out in the ship painting, it will eventually hold other assets too. These assets would start fully backed, but in the case of the underlying asset dropping in value, then the represented asset would be under-backed. However, when there exist leveraged loans in the system, then those would be over-collateralized. Those would be built on top of Gyro.

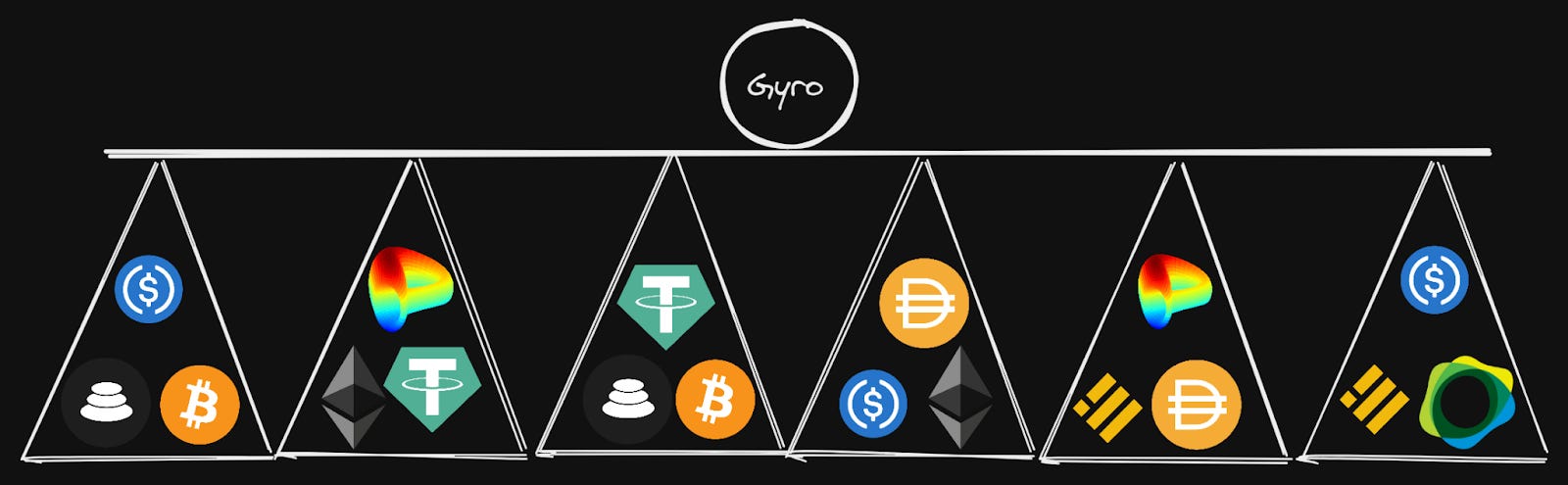

These vaults exist to provide contained risks and should have as little overlap between each other as possible. This means that in the event of a failure of a vault, it won’t overflow to the other vaults. Even in the event of a vault failing, the system will still remain stable through the autonomous price bounding, which is backed by unaffected reserves. These reserves also serve to gain yield on assets, which eventually will lead to the reserve recovering back to its original strength.

This can also be explained in the form of triangles holding a plank, let’s draw out an example:

The reason for this is to isolate risk as much as possible so that if a problem occurs it won’t cascade into other vaults. This means that the reserve of Gyroscope is separated into vaults (the triangles) that help contain risks. Such that if there’s a failure or cascade in one of the vaults, it won’t contaminate the rest. If a vault fails, then the dynamic price bounding which is backed by the rest of the reserve kicks in to help keep the peg.

Further Measures

The second line of defence is the one I just mentioned, dynamic pricing. In the event that a stablecoin unit turns undercollateralized, the bonding curve of the redemption market will then start decreasing redemption quotes. This means that it acts as a circuit breaker to maintain stability. This mechanism most likely won’t be used very often, unless in the case of extreme market events. Although, it’s important to secure the stability of the protocol in any situation, and thus Gyroscope aims to maintain stability in any event.

The reason for decreasing redemption quotes is to have it work as a deterrent to bank runs and attacks on the peg. In the same vein, it rewards users who wait out downturns in the market. Although, it is important to remember that while holders can still exit their stable position, there are now reasons to “bet” on the return of the peg to the targeted price. In due time as the redemption price autonomously works to recover towards peg, outflows will turn towards zero or through the reserve recovering through yield.

There also exist other stability mechanisms that can help stabilize the peg. One of them is because Gyro works similar to the way Maker’s Peg Stability Module operates. However, it does have some different functionalities. While Gyroscope allows for the exchange of its stable with $1 worth of assets, it does also allow for the ability to diversify risks in the reserve backing the stable. Furthermore, in the long term, it won’t be primarily backed by custodial stablecoins (such as the 70% USDC backing DAI). It also allows for the ability to flexibly survive depeg events, even in the event of a fluctuating reserve.

This is through a leveraged loan mechanism that kicks in, in the event of the reserve becoming under-collateralized. If the price of the stable falls under the peg significantly (during a market crash for example), then leverage loan holders will be able to deleverage their positions at a discount. This will reduce the supply of the stable and help the price of the stable return towards $1 (This is quite similar to the way MIM operates — MIM always assumes 1MIM is $1, even if the price falls under the peg, and allows for the ability to redeem $1 of assets for 1MIM).

The Last Resorts

Last resort is used only when all else has failed. The way last resorts works on Gyroscope is that the reserve can also be recapitalized through the auctioning of governance tokens or the promise of future protocol-derived income from the reserve or trading fees. This is quite similar to the way Maker’s backstop works and is only supposed to only happen in the event of last resort during a difficult crisis, through governance. In the same vein, while the prices are good and the valuation of the governance token is high, governance of the protocol is also incentivized to auction off tokens early on to boost the reserve for darker times. This is similar to the way Frax operates by utilising FXS to control the peg in harsh market conditions. However, unlike with the FRAX/FXS mechanisms, this is a tertiary line of defense in Gyroscope, not a 1st line of defense as with Frax.

Oracle Feeds

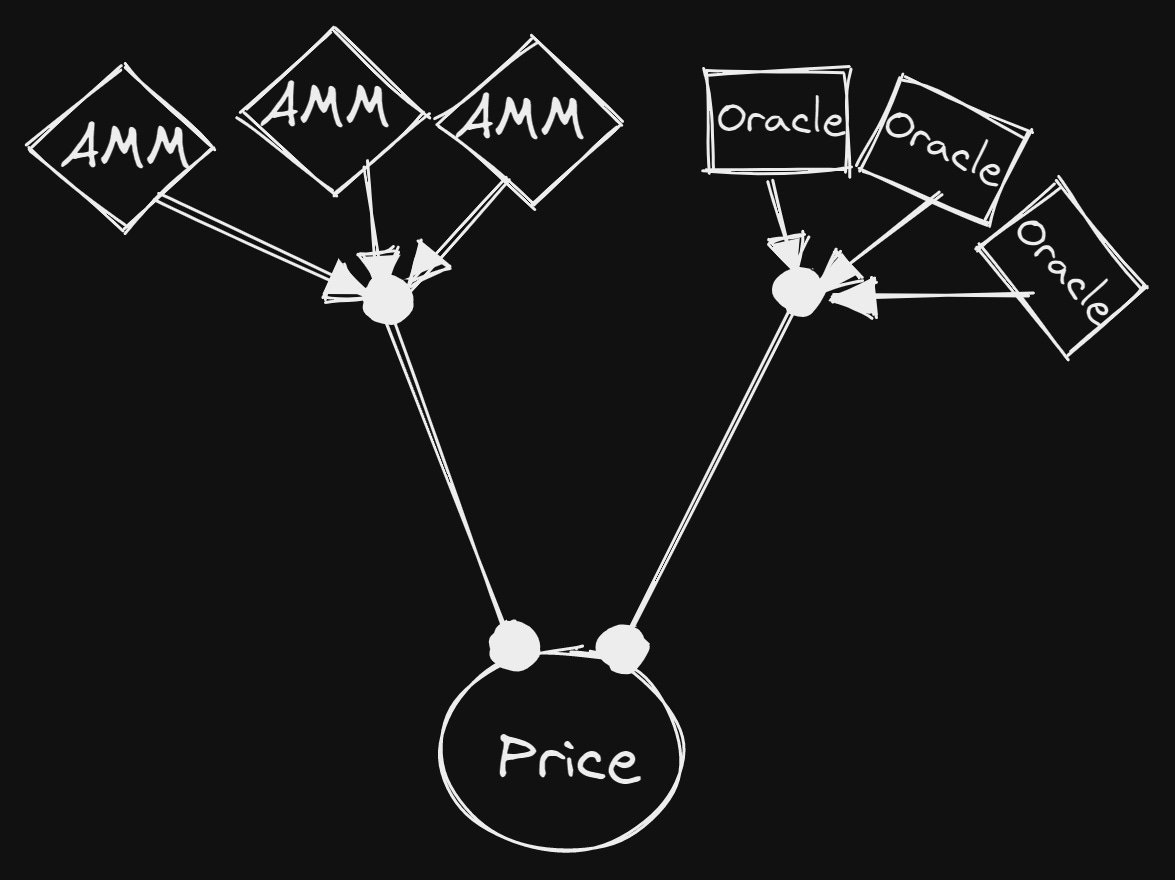

The way Gyro’s oracle feeds work is quite different from other protocols. They rely on several on-chain consistency checks as well as circuit breakers and manipulation-resistant methods for pricing LP and shares of the vaults. Here of particular importance, are the Consolidated Price Feeds. Correct price feeds are extremely important when the stablecoin is being used in DeFi. A great example is, that during the UST fiasco several protocols were exploited as their oracle provided the wrong information on the price of UST. This consequently allowed exploiters to seize advantage of incorrect prices to take out huge loans. The same goes for the latest Inverse Finance exploit, which also made use of bad oracles. The exploiters manipulated the price of a single oracle, which fed info to the protocol.

Layered Price Feeds are when you get on-chain references from AMMs and then ground the price received from AMMs by cross-referencing it with several oracles.

Therefore by layering prices from various sources you can easily detect discrepancies and issues on-chain. This also means that manipulating the prices would take a huge amount of capital across several platforms to have an effect. If a discrepancy is detected the system can stop trading and wait for the issue to be resolved. Most projects usually just rely on a single oracle provider for their price feeds, this is much more exploitable.

Dynamic pricing and beyond

Before we continue onwards to the unique governance mechanics of Gyroscope let’s dig a bit deeper into the dynamic pricing modules of Gyroscope and what they can enable for the protocol.

Gyroscope makes use of two unique and different automated market mechanisms. The first one is the Dynamic Stability Mechanism (DSM), which works to quote the minting and redeeming prices of stables while accounting for shocks to the assets that back the stable.

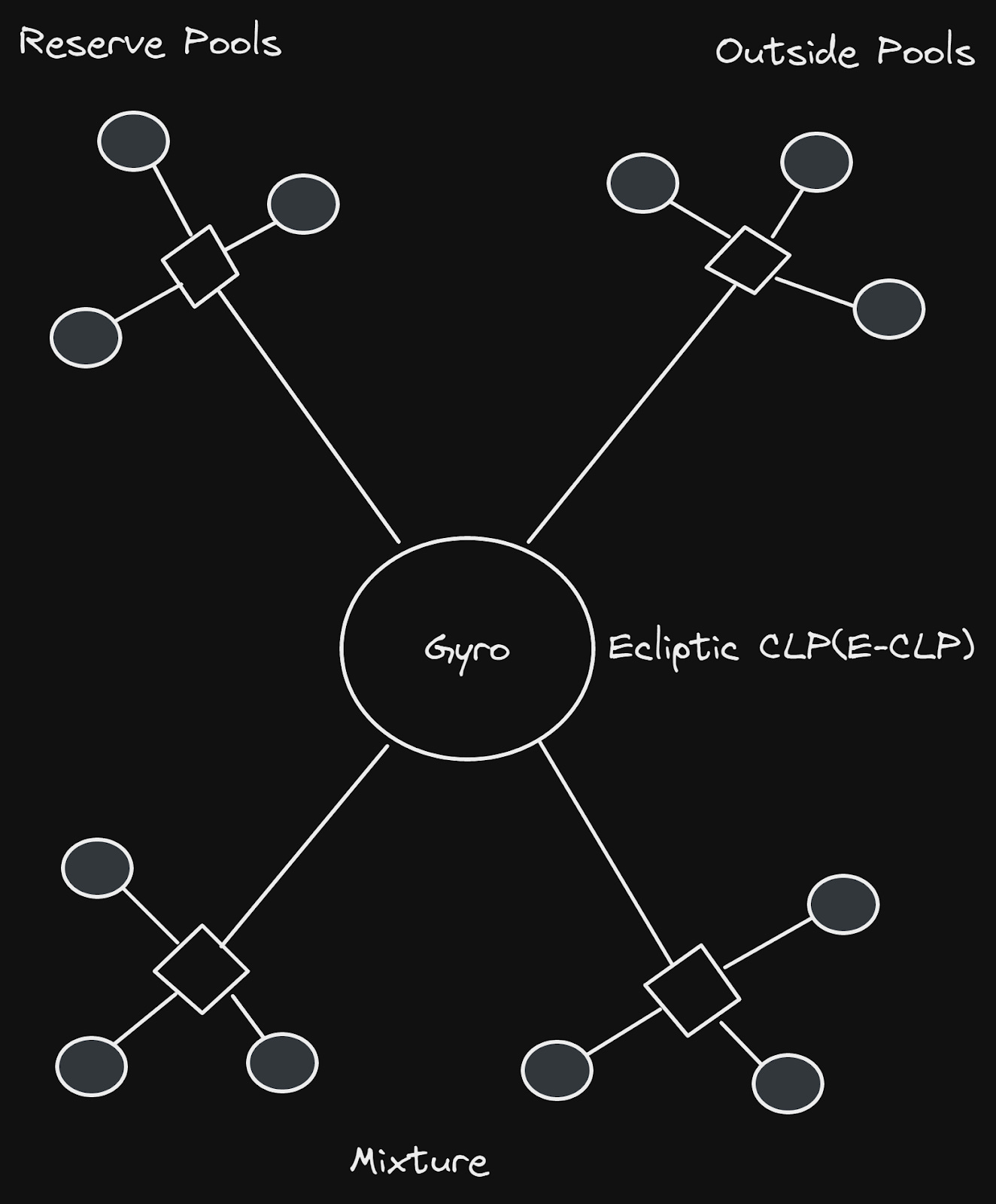

The second pricing module is the Concentrated Liquidity Pools (CLPs) that help to concentrate liquidity within particular pricing bounds through customized Balancer v2 pools. This is done through a partnership with Balancer, which will allow for the logic needed for the customized AMMs.

The CLPs concentrate liquidity where needed according to the information that is given by the DSM for the stablecoin pairs backed by Gyroscope’s reserve assets. CLPs are like Uniswap v3 but on Balancer and specialized to the most-traded range. This means that there will also be liquid paths both in and out of stablecoins from Gyro. Furthermore, the CLPs are independent, which means that just as with the stratified reserve any failures won’t affect the rest.

These pricing modules enable some rather unique designs when it comes to building things beyond the basic mechanics of the Gyroscope protocol. It enables building a DEX that can withstand asset failures through the Gyroscope design, something that Osmosis could have made use of quite efficiently during the UST fiasco.

The design allows for secondary markets to act as AMMs, Reserve Pools and so on, which can route trades as efficiently as possible. In essence, the various pools would look something like this from a birds-eye perspective.

Once Gyroscope has accumulated a strong enough reserve with the widespread acceptance of the stablecoin itself, it will in any market situation be stable at $1. During extreme events, it’s possible that the peg could vary, however, the system by design is made so that such an event is extremely unlikely. Even in the event of a short-term depeg, the stratified reserve and yield mechanisms will aid the stable in the recovery to its peg.

Gyroscope is also trying to innovate on the governance front by implementing a new governance system called Optimistic Approval. Optimistic Approval aims to help align the governors of the protocol with the long-term interest of the protocol itself. So instead of being focused on the short-term and rapid ideas and concepts, the governance of Gyroscope will help to tie the best interest of the protocol together with the governors.

So this is all fine and dandy, but how can we make sure that the governors can’t abuse their power in other ways? This is especially pivotal, when you look at the last few months and how some of the governance proposals taken by Solend and Juno have turned out.

Optimistic Approval

Optimistic Approval is a new form of governance proposed by the Gyroscope team that incorporates a veto mechanism into the governance of the protocol. Which is invokable by other parties in the system like vaults, stablecoin holders and so on, in the event of malicious governance proposals (something that I’m sure SOL holders wish they would have had during the Solend proposal).

The reason for the adding of a veto is that it lowers the success probability of a governance-based attack, since if the malicious attackers are expecting a veto to be put in place, then the chances of this attack happening, to begin with, are already lowered by a wide margin.

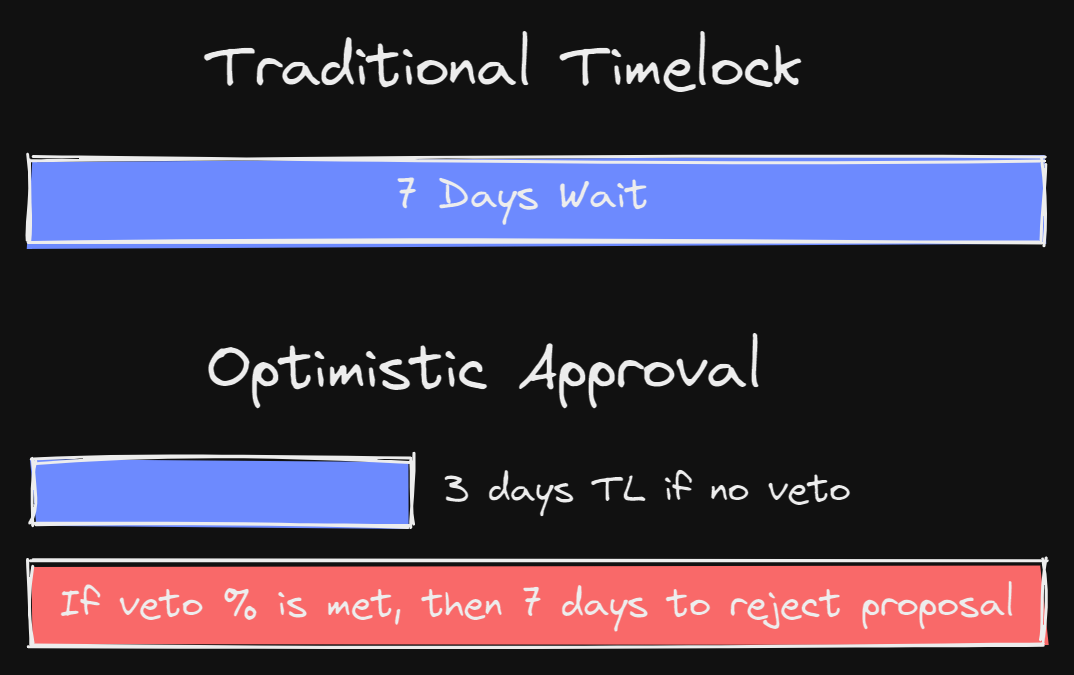

Optimistic Approval relies heavily on the concept of timelocks and is indeed derived from it. Optimistic Approval enables proposals to be quickly passed unless a veto is initiated by some party. These parties could be members of the community at large, so not necessarily governance token holders, but rather other players that use the protocol such as a vault or stablecoin holder like DAI holders, LPs etc. If a situation arises where the minimum required number of users initiates a proposal veto, then the original timelock duration is then increased to enable more users to voice their opinion via voting for or against it. This means that unlike the majority of other protocols, Gyroscope is able to ship updates rather frequently, while still giving the wider community a chance to partake in the governance of the protocol.

The two major reasons for the implementation of optimistic approval are that it enables recourse. Let’s say that a malicious upgrade is being passed in a timelock-based protocol's governance forum, it will lead to the holders running for the exits. However, the chance of vetoing leaves actions on the table for the community.

Likewise, it also acts as a fail-safe of the protocol. In the event of another malicious proposal, an absentee user doesn’t need to worry about losing funds (cough Solend), since only a small number of users are required to increase the timelock and keep the protocol safe.

However, there’s obviously one contrarian view on the concept of optimistic approval and that is determining what “the wider community” entails when it comes to being allowed veto powers to extend the timelock. Does this apply to holders of debt positions on protocols like Maker which allows for the minting of DAI, or should it lie in with the holders of DAI or MKR itself? There’s also the possibility of a wider community member wanting to fight against a proposal being implemented quickly and extending the timelock through vetoing. One thing that's very important to remember is, that there are many vital voices beyond large token holders, and basic token-based voting mechanisms might not incorporate them. Optimistic Approval helps alleviate some of these issues with current governance in crypto protocols, and it would be great to see more protocols utilise a similar scheme.

Here’s how a timelock could look from a protocol using a traditional governance method, and how an Optimistic Approval-based timelock works on Gyroscope.

This means that Optimistic Approval gives users and token holders of the protocol the ability to veto changes that they disagree with, as long as they meet a certain quorum. As such the stability of the protocol is ensured, since it adds checks and balances on the power of those who hold the governance token, ensuring that no malicious crypto-economic attacks are carried out by actors acting against the long-term interest of the protocol. This should of course always tie into the concept of allowing governors of the protocol to earn sufficient profit or other positives so that it outweighs the expected proceeds from a possible crypto-economic attack on the system itself.

Stablecoins are incredibly important for the wider crypto ecosystem since they allow for the linking of the traditional financial world and the decentralized world of crypto. It furthermore enables the ability to have USD-Token pairs on DEXs, which is also something that’s very vital. In risk-off periods to which crypto is very prone, the ability to seek shelter in safe and uncompromising stablecoins is also vital for the health of the ecosystem.

Stablecoins are also a vital key to unlocking global transactions that can’t rely on volatile assets. The nature of blockchains means that these transactions can be enabled with extremely low transaction fees and fast settlement.

Furthermore, we have seen an increased interest in having stablecoins used for cross-border payments and remittances from traditional finance players such as JP Morgan and Wells Fargo. This means that we could see a possible future where stablecoins are used to cut out intermediary financial institutions and enable truly global payments. However, if such a future is to exist it needs to be with a governance mechanism that is aligned with the long-term health of the protocol, as with Gyroscope.

The scalability of the stablecoin is also extremely important. We saw how UST and many other stablecoins outgrew their internal risk absorption mechanisms, which eventually led to their downfall. With the stratified reserve of Gyroscope, we are no longer constrained by a single system and can rather grow stablecoins as DeFi itself evolves.

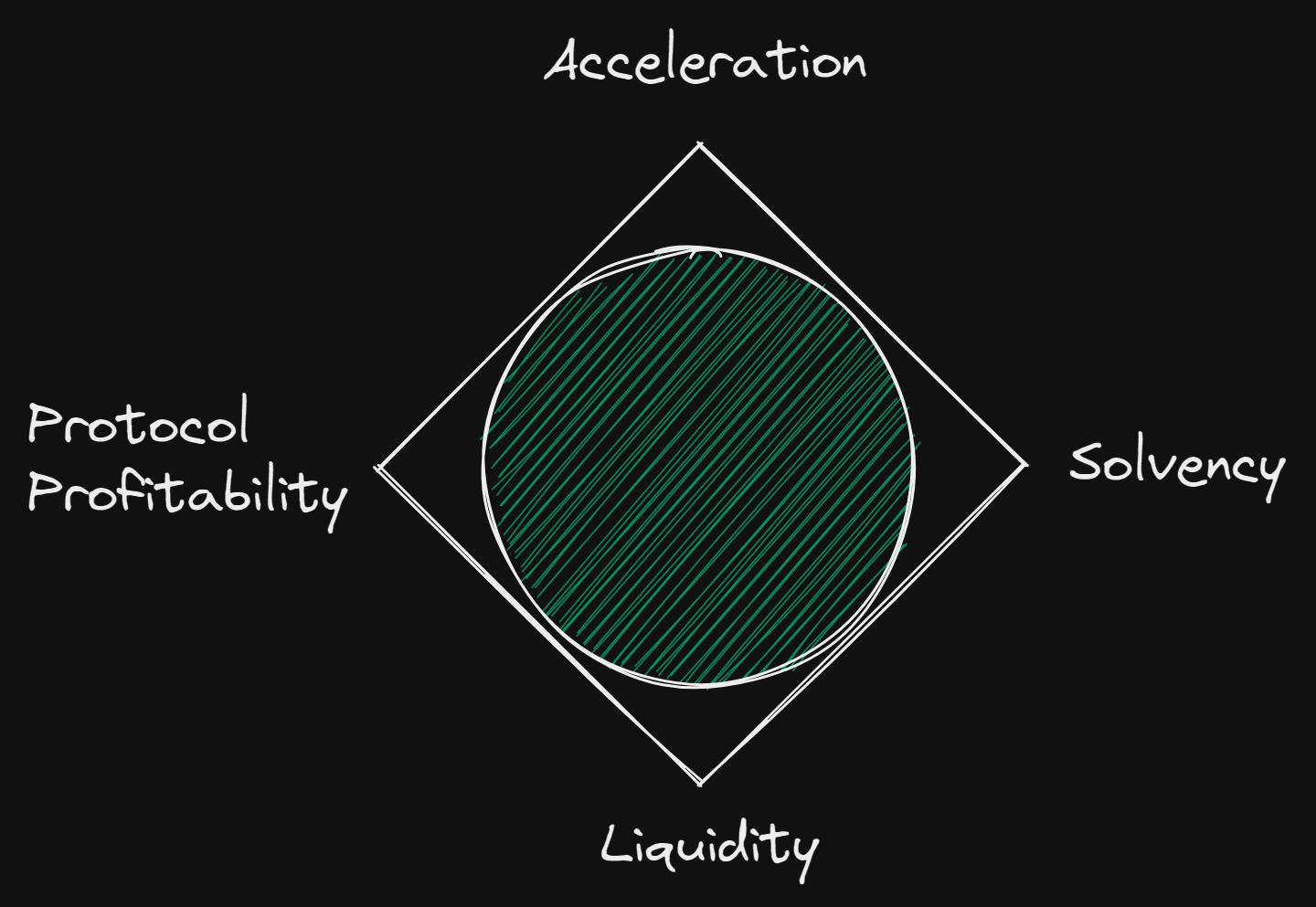

For an “algo” stable to truly succeed it needs four major functionalities

It is also of absolute importance that the backing of the stablecoin is majorly exogenous, we’ve seen how a primary endogenous backing can have extremely negative effects during market shocks.

We believe that Gyroscope has the ability to solve these four major hurdles and we’re extremely excited to see where the future of Gyroscope takes us.

.jpg)